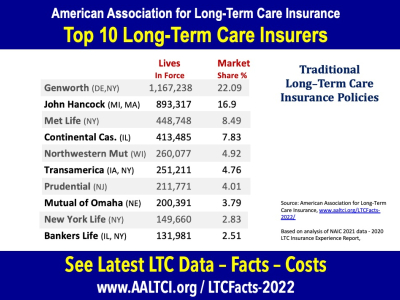

Mutual of Omaha, New York Life, and Genworth Financial are among the best long-term care insurance companies. They offer comprehensive coverage and financial stability.

Long-term care insurance helps cover the costs of services that assist with daily activities. These services can include home care, assisted living, and nursing home care. Choosing the right insurance company ensures peace of mind and financial security. Mutual of Omaha is known for its flexible plans and strong customer service.

New York Life offers customizable policies and excellent financial ratings. Genworth Financial provides extensive options and competitive rates. Evaluating these companies based on coverage, cost, and customer reviews is crucial. Proper research helps in selecting a plan that best suits individual needs and future requirements.

Introduction To Long-term Care Insurance

Long-term care insurance helps cover costs for extended care services. These services may include help with daily activities like bathing, dressing, and eating. As people age, the need for long-term care increases. This insurance can protect your savings and provide peace of mind.

The Need For Long-term Care Coverage

Many people will need long-term care at some point. Without insurance, the costs can be high. Long-term care insurance helps pay for these expenses. It ensures you get the care you need without burdening your family. This coverage can be used at home, in assisted living, or in nursing homes.

Criteria For Selecting Top Insurance Companies

Choosing the best long-term care insurance company is crucial. Consider these factors:

- Financial Strength: Ensure the company is financially stable.

- Customer Service: Check reviews and ratings for customer support.

- Policy Options: Look for flexible and comprehensive plans.

- Claim Process: A simple and quick claim process is essential.

- Cost: Compare premiums and benefits to find the best value.

| Company | Financial Strength | Customer Service | Policy Options | Claim Process | Cost |

|---|---|---|---|---|---|

| Company A | Excellent | 4.5/5 | Wide Range | Fast | $$$ |

| Company B | Good | 4/5 | Flexible | Moderate | $$ |

| Company C | Very Good | 4.7/5 | Comprehensive | Quick | $$$ |

The Landscape Of Long-term Care Insurance

Long-term care insurance is critical for aging populations. It covers costs related to care services. These services range from home care to nursing homes. The industry has evolved significantly in recent years.

Current Trends In Long-term Care Insurance

Several trends are shaping the long-term care insurance market. One major trend is the rise of hybrid policies. These policies combine life insurance with long-term care benefits. They offer more flexibility and value.

Another trend is the shift towards personalized care plans. Insurers now offer plans tailored to individual needs. This customization ensures better coverage and satisfaction.

The use of technology is also increasing. Telehealth services and digital tools help manage care effectively. They provide easier access to necessary services.

Challenges In The Market

The long-term care insurance market faces several challenges. One significant challenge is the high cost of premiums. Many people find it difficult to afford these policies.

Another challenge is the aging population. As more people age, the demand for long-term care rises. This increases pressure on the insurance industry.

There is also a lack of awareness about the importance of long-term care insurance. Many people do not understand the benefits. This results in lower adoption rates.

Lastly, there are regulatory challenges. Different states have different regulations. This makes it hard for insurers to offer uniform policies.

Factors To Consider When Choosing A Provider

Choosing the best long-term care insurance company is crucial. You want to ensure your needs are met. This section will guide you through essential factors.

Coverage Options

Different companies offer various coverage options. It’s essential to know what each plan includes.

- Daily Benefits: How much the plan pays per day for care.

- Benefit Period: The length of time benefits are paid.

- Inflation Protection: Keeps your benefits in line with inflation.

Premium Costs

Premium costs can vary widely. It’s important to compare.

| Company | Monthly Premium |

|---|---|

| Company A | $150 |

| Company B | $200 |

Consider how premiums fit into your budget. Look for any discounts that may be available.

Company Stability And Ratings

Ensure the company is stable and has good ratings. This helps ensure they will be around when you need them.

- Financial Stability: Check ratings from agencies like A.M. Best.

- Customer Reviews: Look at what other customers are saying.

- Claim Process: Ensure they have an easy claim process.

Choosing a stable company gives you peace of mind. Ratings and reviews can provide valuable insights.

Top Picks For Long-term Care Insurance

Choosing the right long-term care insurance is crucial for your future. It provides peace of mind and financial security. Here, we highlight the top picks for long-term care insurance. This guide will help you identify the best options available.

Industry Leaders In Long-term Care

These companies are renowned for their strong reputations and comprehensive coverage.

| Company | Key Features |

|---|---|

| Genworth Financial |

|

| Mutual of Omaha |

|

| New York Life |

|

Emerging Companies To Watch

These companies are newer but offer competitive and innovative solutions.

| Company | Key Features |

|---|---|

| Golden Care |

|

| National Guardian Life |

|

| Bright house Financial |

|

In-depth Reviews Of Selected Companies

Choosing the right long-term care insurance can be challenging. Let’s explore some top-rated companies offering the best coverage and customer service. These in-depth reviews will help you make an informed decision.

Company 1: Comprehensive Coverage Review

Company 1 is known for its comprehensive coverage. They offer a wide range of services to meet various needs.

- Home Care: They provide extensive home care options.

- Nursing Home Care: Top-rated services for nursing home care.

- Assisted Living: Reliable assisted living facilities.

Their policy options are flexible. You can choose different levels of coverage to fit your budget. They also offer inflation protection to ensure your benefits keep up with rising costs.

| Feature | Details |

|---|---|

| Home Care | Extensive services available |

| Nursing Home Care | Top-rated facilities |

| Assisted Living | High-quality options |

| Inflation Protection | Available |

Company 2: Customer Service Excellence

Company 2 excels in customer service. Their support team is available 24/7 to answer questions and address concerns.

Their claims process is straightforward. Customers report quick and hassle-free claims. They offer online tools to manage your policy easily.

- 24/7 Customer Support

- Quick Claims Process

- Online Policy Management

They have received high ratings for customer satisfaction. Most clients are happy with their service and recommend them to others.

Company 2 is committed to providing the best experience for their policyholders. Their dedication to customer service sets them apart.

Credit: money.com

Comparing Policies: What To Look For

Choosing the best long-term care insurance company is crucial. Different policies offer various benefits. Knowing what to look for helps you make the best choice.

Benefit Periods And Daily Benefits

Benefit periods determine how long the insurance will pay. Some policies offer coverage for a few years. Others provide lifetime benefits.

| Benefit Period | Description |

|---|---|

| 2-5 Years | Covers short to medium-term needs |

| Lifetime | Covers long-term or permanent needs |

Daily benefits are the amounts paid per day. Higher daily benefits mean more coverage. Choose according to your needs.

- Low Daily Benefit: Covers basic needs

- High Daily Benefit: Covers extensive care

Inflation Protection

Inflation protection increases your benefits over time. It keeps up with rising care costs. There are two main types:

- Automatic Inflation Protection: Increases benefits automatically

- Optional Inflation Protection: Allows you to increase benefits as needed

Choosing inflation protection is essential. It ensures your policy stays valuable over time.

Elimination Periods

The elimination period is the waiting time before benefits begin. This period can range from zero to 180 days.

| Elimination Period | Description |

|---|---|

| 0-30 Days | Short waiting period, higher premiums |

| 60-90 Days | Moderate waiting period, moderate premiums |

| 180 Days | Long waiting period, lower premiums |

A shorter elimination period means quicker access to benefits. A longer period can lower your premiums.

Understanding these key factors helps you choose the best policy for your needs.

Customer Experiences And Testimonials

Choosing the best long-term care insurance company can be challenging. Customer experiences and testimonials provide valuable insights. They highlight how companies treat their customers. Let’s explore the feedback and claims handling of top companies.

Positive Feedback Highlights

Positive reviews play a crucial role in decision-making. Happy customers often praise the service quality and support.

- Company A: Customers love the quick response times.

- Company B: Many appreciate the affordable premiums and comprehensive coverage.

- Company C: Users highlight the helpful and knowledgeable staff.

These positive experiences build trust and confidence among potential buyers.

Handling Of Claims And Disputes

How a company handles claims and disputes is critical. Efficient claims processes ensure peace of mind for policyholders.

| Company | Claims Process | Dispute Resolution |

|---|---|---|

| Company A | Fast and hassle-free claims processing. | Quick resolution of disputes. |

| Company B | Clear and transparent claims guidelines. | Effective dispute resolution mechanisms. |

| Company C | Customer-friendly claims support. | Responsive dispute management. |

Reliable claims and dispute handling are essential for customer satisfaction. These companies excel in these areas, making them top choices.

Credit: www.insuranceandestates.com

Finding the best long-term care insurance can be complex. Understanding the fine print is crucial. This section breaks down key points to consider.

Understanding Exclusions And Limitations

Insurance policies often have exclusions and limitations. These are conditions or situations not covered by the policy.

- Pre-existing Conditions: Many policies do not cover pre-existing conditions.

- Waiting Periods: Some policies have waiting periods before benefits begin.

- Benefit Triggers: Benefits may only start after specific conditions are met.

Always read the exclusions and limitations. This ensures you understand what is covered.

Renewability And Portability Features

Renewability and portability are vital features. These determine how long the policy lasts and if it moves with you.

| Feature | Description |

|---|---|

| Guaranteed Renewability: | The insurer cannot cancel your policy if you pay the premiums. |

| Portability: | You can move to another state without losing your coverage. |

Check these features carefully. They offer peace of mind and flexibility.

Future Of Long-term Care Insurance

The future of long-term care insurance looks promising with new innovations. Companies are striving to provide better and more comprehensive coverage. Consumers can expect a range of benefits and advancements in this sector.

Innovations In Coverage

Long-term care insurance is evolving with several new features. Insurers are now offering hybrid policies that combine life insurance with long-term care benefits. These policies provide more flexibility and financial security.

Another significant innovation is the inclusion of home care services. Many prefer receiving care at home instead of a facility. This change caters to that need, providing coverage for home health aides, therapy, and more.

Technological advancements are also playing a role. Some policies now cover the costs of telehealth services. This allows policyholders to receive medical advice and monitoring remotely.

Predictions For The Insurance Industry

The insurance industry is expected to see several changes in the coming years. One key prediction is the rise of customizable policies. Consumers will have the option to tailor their coverage according to their specific needs.

Another prediction is the increased use of artificial intelligence in underwriting and claims processing. AI can help streamline these processes, making them faster and more efficient.

Lastly, there is likely to be a shift towards preventive care coverage. Insurers may start covering services that help prevent the need for long-term care, such as wellness programs and regular health check-ups.

| Innovation | Benefit |

|---|---|

| Hybrid Policies | Combines life insurance and long-term care benefits |

| Home Care Services | Covers in-home care options |

| Telehealth Services | Provides remote medical consultations |

| Customizable Policies | Allows tailoring of coverage |

| Artificial Intelligence | Streamlines underwriting and claims processes |

| Preventive Care Coverage | Supports wellness and health check-ups |

Conclusion: Making An Informed Choice

Choosing the right long-term care insurance is crucial. It impacts your future and finances. This section helps you make an informed choice.

Recap Of Top Picks

Here are the top long-term care insurance companies:

- Genworth Financial: Known for flexible plans and extensive coverage.

- Mutual of Omaha: Offers affordable rates and great customer service.

- Northwestern Mutual: Renowned for financial strength and stability.

- New York Life: Provides customizable plans and excellent support.

- Transamerica: Focuses on diverse plan options and affordability.

These companies stand out for their unique features and benefits. Each has its strengths and weaknesses.

Final Thoughts On Selecting A Provider

Consider these factors when selecting a provider:

- Coverage Options: Make sure the plan covers your needs.

- Cost: Compare premiums and benefits across providers.

- Customer Service: Look for companies with high customer satisfaction.

- Financial Stability: Choose a provider with strong financial ratings.

- Flexibility: Ensure the policy can adapt to your changing needs.

Making an informed choice means balancing cost, coverage, and service. This way, you secure your future with confidence.

| Company | Strengths | Weaknesses |

|---|---|---|

| Genworth Financial | Flexible plans, extensive coverage | High premiums |

| Mutual of Omaha | Affordable rates, great service | Limited plan options |

| Northwestern Mutual | Financial strength, stability | Expensive |

| New York Life | Customizable plans, excellent support | Higher premiums |

| Transamerica | Diverse plan options, affordability | Averages customer service |

Credit: www.ssltc.com

Frequently Asked Questions

What Is The Biggest Drawback Of Long-term Care Insurance?

The biggest drawback of long-term care insurance is its high cost. Premiums can increase significantly over time.

What Is The Oldest Age For Long-term Care Insurance?

The oldest age to buy long-term care insurance is typically 79. Eligibility and premiums may vary by provider.

What Are The Three Main Types Of Long-term Care Insurance Policies?

The three main types of long-term care insurance policies are traditional long-term care insurance, hybrid life insurance, and long-term care annuities.

Who Would Most Likely Need Long-term Care Insurance?

Older adults, individuals with chronic illnesses, or those with a family history of long-term care needs would most likely need long-term care insurance.

Conclusion

Choosing the right long-term care insurance is crucial for your future. Research the best companies to find the perfect fit. Prioritize coverage options, customer service, and affordability. Secure peace of mind with a policy tailored to your needs. Plan ahead and ensure financial stability in your later years.